AIAIG Opinion2026年3月8日

New Zealand's Active Investor Plus Visa: 2025-2026 Policy Changes and...

New Zealand's 'Golden Visa' typically refers to the Active Investor Plus Visa, a long-term residency pathway for high-net-worth individuals. During 2025–2026, the New Zealand government adjusted this visa system, with the core goal of attracting more long-term capital and innovative investments, rather than passive funds. This article systematically outlines: the two investment channels for the Active Investor Plus Visa (growth investments and balanced investments), investment amounts and residency requirements, funding sources and approval processes, as well as the practical impacts of policy changes on investors from China, Hong Kong, and the United States.

Read More

AIAIG Opinion2026年3月8日

Thailand Land Buying Guide: Understanding Color Zoning (Purple/Red/Yellow/Gre...

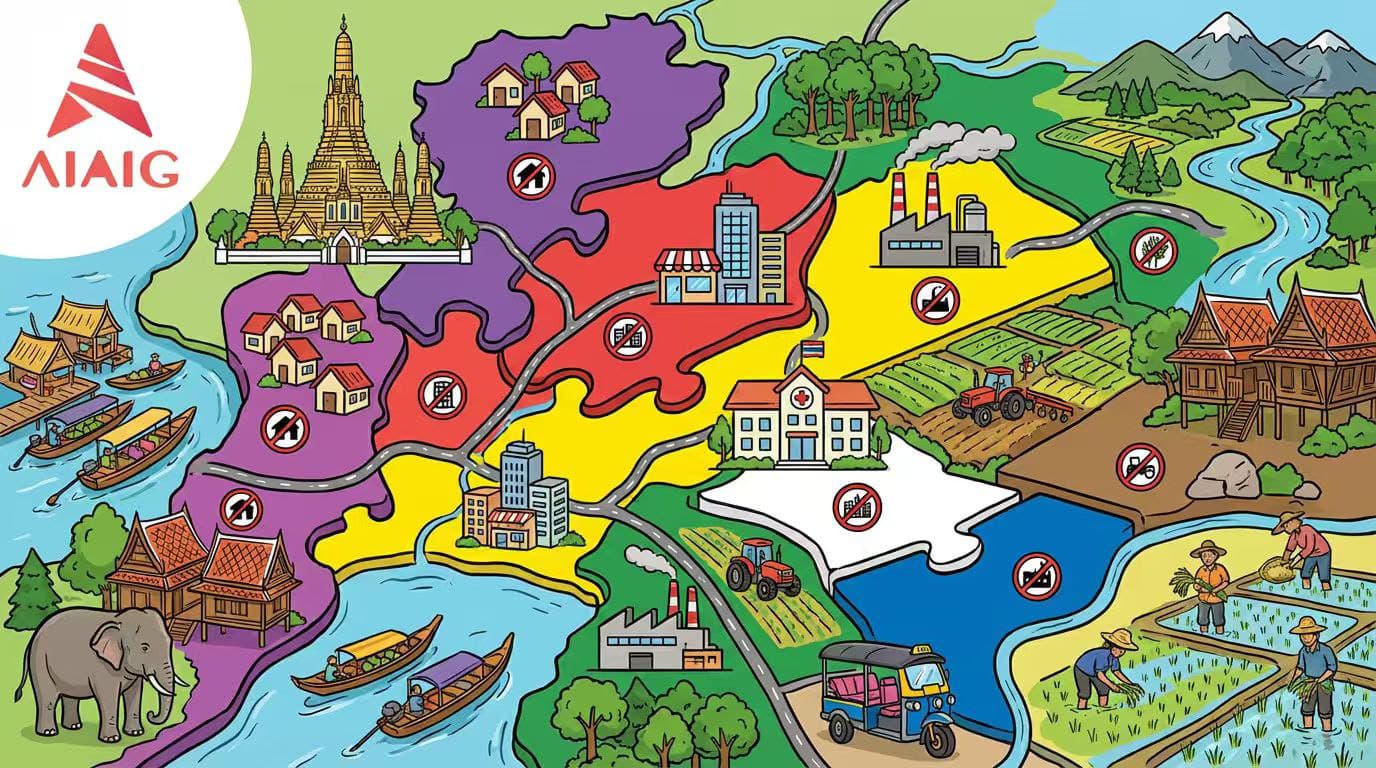

When buying land in Thailand, the biggest pitfall isn't the price, but the land use. Thai urban planning often uses 'color zoning' to indicate land purposes, such as industrial, commercial residential, low-density residential, agricultural, and conservation areas. Many foreign buyers or first-time investors overlook this, leading to land that cannot be developed or has restricted uses. This article systematically outlines common Thai land color zoning: what each color represents, what buildings are allowed, typical locations, and key documents and approval processes investors must check before purchasing.

Read More

AIAIG Opinion2026年3月6日

Japan's Land and Tourism-Driven Housing Price Rise: Where Are the Next...

The recovery of Japan's housing and land prices in recent years is not driven solely by a 'nationwide surge,' but by three overlapping forces: inbound tourism recovery, redevelopment and transportation hub upgrades, and capital revaluation of local industries and resort economies. This article avoids emotional hype about 'hotspot cities' and instead uses official land price announcements, JNTO tourism statistics, and public project trends to analyze: why tourism boosts commercial and residential land, what types of cities are more likely to transform 'tourism heat' into 'housing and land price elasticity,' and which areas, despite high popularity, also face risks of overheating, seasonality, and resident backlash.

Read More

AIAIG Opinion2026年3月5日

Japan's Latest Policies for Attracting Foreign Talent and Tech Immigration:...

Japan's recent 'talent attraction' efforts are not just about visa relaxation but involve multiple pathways for different groups: high-skilled (Highly Skilled Professional/J-Skip), mid-skilled in shortage occupations (Specified Skilled Worker), short-term remote workers (Digital Nomad Designated Activities), and business/management visas (Business Manager) that emphasize 'genuine business and employment contributions' amid stricter regulations. This article uses a tool-based framework to outline: each pathway's positioning, key thresholds, available residency and family arrangements, renewal/long-term status logic, and practical impacts of 2025–2026 regulatory adjustments on 'tech immigration planning'.

Read More

AIAIG Opinion2026年3月4日

2026 Asia Real Estate & Infrastructure Summit Highlights: EXPO REAL (Munich)...

As of March 2026, WCS (World Cities Summit) has announced its 2026 theme and agenda framework, linking with 'EXPO REAL Asia Pacific' and 'Asia Infrastructure Forum'; EXPO REAL (Munich) has also confirmed its 2026 dates and core topics. This article, in a 'tool-based hot topics delivery' style, breaks down public information from both platforms into actionable checklists for participation and investment analysis: which sectors are likely to be focal points (AI and urban governance, green finance, urban renewal and housing, data centers and infrastructure, etc.), which content is more likely to translate into policies and funding implementation, and the Q&A and due diligence indicators that investors/developers/institutions should prepare before the events.

Read More

AIAIG Opinion2026年3月3日

4 Structural Trends in Southeast Asia's Real Estate: Remote Work,...

The main drivers of Southeast Asian real estate are no longer just 'demographic dividend + urbanization,' but are being reshaped by four structural variables: remote/hybrid work changes living radii and office differentiation; rail transit and regional connectivity upgrades alter land price gradients; AI and data centers bring new industrial real estate and power constraints; climate risks, energy consumption, and insurance costs are being repriced. This article breaks down each trend's mechanisms, impacts on residential/office/logistics/industrial parks, and actionable indicators and checklists for investors.

Read More

AIAIG Opinion2026年3月2日

Southeast Asia 8-Country Investment Immigration Comparison: Minimum...

Breaking down 'Southeast Asia investment immigration,' you'll find most countries offer 'long-term residency/visas' rather than immediate permanent residency or citizenship. This article uses a single comparison table to horizontally compare Singapore, Malaysia, Thailand, Indonesia, Philippines, Vietnam, Cambodia, and Laos across eight aspects: minimum capital thresholds, available resident rights (work/business/bring family/buy property, etc.), pathways for renewal and conversion to permanent residency (or long-term status), and key restrictions (stay duration, fund lock-in, compliance reviews, non-transferable clauses).

Read More

.jpg&w=3840&q=75)

AIAIG Opinion2026年3月2日

Singapore Real Estate Investment Trends: Post-Pandemic Office Market Recovery...

In 2026, Singapore's commercial real estate narrative is shifting from 'post-pandemic recovery' to 'supply-demand rebalancing': office space is once again becoming a preferred asset class for investors, with capital increasingly concentrated in high-quality (Grade A) buildings in the core CBD. This article uses a tool-based framework to analyze: what the office recovery entails (flight-to-quality and core resurgence), why the core CBD attracts more capital (liquidity/financing/lease certainty), and how investors can use quantifiable metrics to select assets while avoiding risks from 'aging offices' and refinancing.

Read More

AIAIG Opinion2026年2月28日

Singapore GIP 2026: Investment Paths, PR/Citizenship Planning

Singapore's Global Investor Programme (GIP) is essentially 'trading genuine business/capital commitments for PR pathways.' By 2026, three investment options are available: A (business investment S$10m), B (GIP fund S$25m), C (family office AUM≥S$200m with at least S$50m transferred and deployed as required). This article uses a tool-based framework to analyze: target groups, thresholds and materials, timeline from AIP to final PR, hard indicators for REP renewal, and key planning points and common pitfalls for 'PR→citizenship' in practice.

Read More

AIAIG Opinion2026年2月28日

2026 Asia Real Estate Investment Trends: Capital Inflows & Asset Allocation...

Multiple institutions are more optimistic about Asia-Pacific commercial real estate in 2026: CBRE forecasts a 5–10% year-on-year increase in investment volume, with office assets regaining top investor preference. Office leasing demand continues to recover, driven by 'prime locations + high-quality buildings'. This article breaks down 2026 capital flows and asset differentiation in a practical, actionable way, offering asset allocation frameworks and risk control checklists for various investors (stable income/family offices/allocative/opportunistic).

Read More